Paraguay’s 1% Tax Model for International Businesses… But What Does This Actually Mean in Practice?

Ralph

4/29/20265 min read

For you as an international entrepreneur or investor, this regime offers a unique ‘early mover’ opportunity. Law No. 7547 is not merely an administrative update, but a strategic instrument designed to stimulate technology transfer and the export of services (Ref: Art. 1 & 2). By entering now, you create significant tax optimization and a sustainable competitive advantage compared to traditional hubs such as Brazil, Uruguay, and more recently Turkey.

‘Early opportunity’ in the Digital Economy

With the enactment of Law No. 7547, Paraguay has firmly positioned itself as the most competitive jurisdiction for cross-border service delivery in Latin America. While the Maquila regime was previously primarily associated with physical assembly, this new legislation marks a paradigm shift toward the 21st-century digital economy.

1. Definition and Application: Export of Services & Value creation

The foundation of Law No. 7547 lies in the broad definition of service exports, provided they are supported by

Paraguayan resources. The following concepts from Article 3 of the law are crucial for strategic planning:

Maquila de Servicios: This regime is specifically designed for operations in which a Paraguayan entity

uses its capacity and processes to provide services to foreign companies. Essential to this is the use of

information and communication technology (ICT) and ‘remotos’ (remote resources), while explicitly generating national added value (Ref: Art. 3h). More on this later.

Exportación de Maquila: Services that are physically performed from Paraguay, but whose economic benefit is enjoyed exclusively abroad, are legally classified as exports (Ref: Art. 3o).

Maquiladora pura vs. por capacidad ociosa:

Pura: An entity established exclusively for export activities under the regime (Ref: Art. 3i).

Capacidad ociosa: An existing Paraguayan company that uses its idle capacity for export

services. Note: For these hybrid entities, specific rules apply regarding the allocation of costs and

taxes (Ref: Art. 3j).

2. The Legal Structure: The Contract and the ‘Matriz’

The operation is legally based on the relationship between the local service provider (Maquiladora) and the foreign client (Matriz).

The Contrato de Maquila: This formal contract establishes the obligations between the Maquiladora and the foreign Matriz (Ref: Art. 3d, 3e).

Carta de Intención (Letter of Intent): The law provides flexibility by allowing the application process to begin with a letter of intent instead of a final contract. However, you must be aware of the strict deadline: if the formal contract is not presented within 180 days after approval of the program, the approval lapses automatically (de pleno derecho) (Ref: Art. 11).

3. The Approval Process: Navigating the CNIME

Obtaining Maquila status requires coordinated approval through the institutional route:

CNIME (Consejo Nacional de las Industrias Maquiladoras de Exportación): This body serves as your primary point of contact and advises the Ministries on your application (Ref: Art. 6, 7).

Biministerial Resolution: The final granting of benefits is made through a joint decision by the Ministry of Industry and Commerce and the Ministry of Economy and Finance (Ref: Art. 5, 8).Long-term

Guarantee: An approved program provides tax certainty for a period of up to 20 years, with the possibility of renewal (Ref: Art. 13).

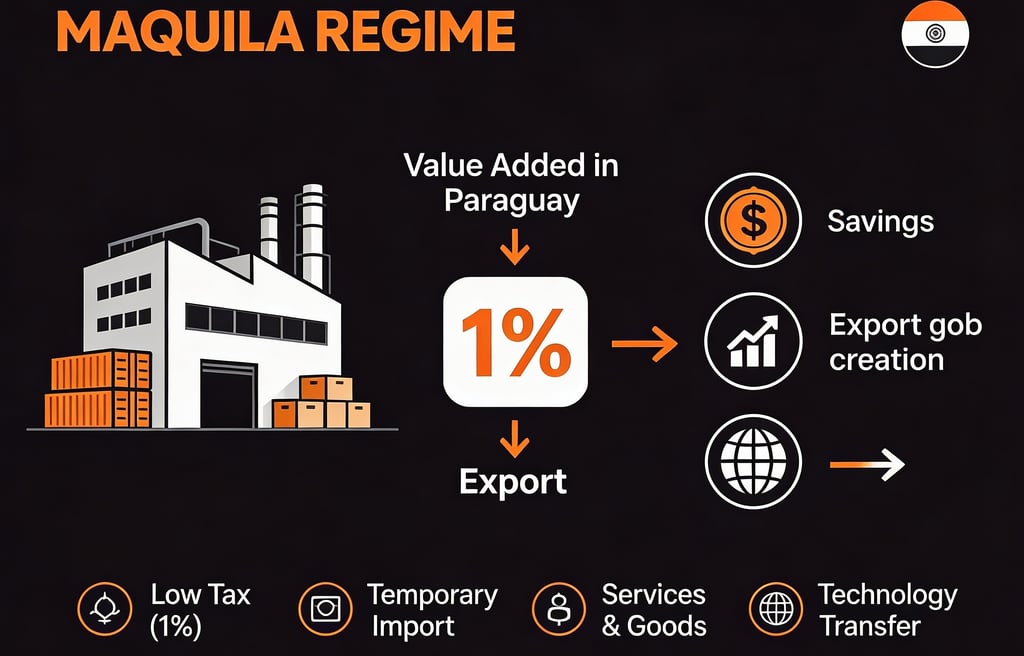

4. The 1% Tax Regime: Analysis of the ‘Tributo Único’

The core of this regime is the highly favorable tax rate, designed to minimize capital flight and maximize local or foreign investment.

The 1% Rule (Tributo Único) applies to export activities. It is calculated on the higher of the following two values (Ref: Art. 37):

The added value generated in Paraguay, or

The total value of the export invoice.

How is the Added Value calculated?Added value includes (Ref: Art. 37a-e):

Locally acquired goods and services

Wages, salaries, and social security contributions of Paraguayan personnel

Depreciation of capital goods owned by the Maquiladora

The fee received by the Maquiladora for its services

Tax Exemptions and Limitations

The law provides extensive exemption from regular taxes on export activities (Ref: Art. 38):

Tax Type Status under Maquila Regime Legal Basis

IRE Exempt Art. 38d

(Corporate Income Tax)

IDU Exempt Art. 38d

(Dividend Tax)

INR Exempt Art. 38d

(Non-Residents)

Import Duties Exempt (Temporary Import) Art. 14

Important note for hybrid entities: If you use the Capacidad Ociosa model (mixed income from local market and export), costs and resulting taxes (IRE, IDU, INR) must be calculated on a pro-rata basis (Ref: Art. 38d).

VAT (IVA) Credit & Exclusions: Maquiladoras can claim a refund of VAT paid on local purchases. However, for service provision, this credit is limited to 0.5% of the added value or export invoice (Ref: Art. 39). Important: The law explicitly excludes “honorarios profesionales” (professional fees) from this refund mechanism. This is a crucial detail for budgeting external consultancy or legal assistance (Ref: Art. 39).5. Operational Obligations and ComplianceTo retain the benefits of the regime, you must comply with strict compliance rules (Ref: Art. 17 & 18):

Staff Training: You are required to invest in the training of local personnel.

Quarterly Reporting: You must report to the CNIME every three months on the progress of the program.

Cuenta Corriente Informático: You must use this specialized digital current account system for comprehensive customs and tax control of your operations.

Domestic Sales: For ‘pure’ Maquiladoras, sales on the local market are limited to 10% of the previous year’s export volume, after payment of the applicable import duties.

6. Risk Management: Tiered Sanctions Structure

The law ensures the integrity of the regime by imposing direct penalties for non-compliance. The fines in Article 33b are specifically structured as follows:

Incorrect destination of goods: Fines of up to 100 minimum wages for using goods or resources under the program for purposes other than those approved.

Essential conditions: Fines of up to 80 minimum wages for failing to comply with the core conditions of the approved Maquila program.

Formal obligations: Fines of up to 60 minimum wages for administrative or material shortcomings.

In case of recurrence, the program may be suspended for up to 6 months or even permanently revoked, resulting in the immediate liability for all regular taxes (Ref: Art. 33c, 33d).

What do we mean by “incorrect destination” of goods or resources? This refers to anything you bring into the company under the Maquila regime, such as:

Machines

Laptops / equipment

Software

Materials

Imported products (often duty-free)

Practical examples of violations:

Importing equipment duty-free but using it for another project

Using resources for local sales (not permitted)

Using resources for activities not included in your approved Maquila plan

Transferring assets to another company

Fines can amount to several thousand up to tens of thousands of dollars. In practice, these are mainly applied in cases of clear system abuse rather than minor errors. Still, it is something to be very conscious of. Always ensure your assets are used strictly in accordance with your approved plan.

7. Conclusion: A Future-Proof Strategy

Law No. 7547 demonstrates that Paraguay is determined to become the digital ‘back-office’ of the world. A key element in this modernization is Article 40, which mandates the digitalization and interconnection of systems between government agencies. This significantly reduces bureaucratic red tape and enables smooth, transparent operations for tech-oriented companies.

Given the stability of the 20-year regime and the extremely low tax burden, I recommend reviewing your current operational structure. The time to establish your legal and fiscal base in Paraguay is now. MyParaWay can support you excellently in this process. Thanks to our strong connections, we ensure the entire setup is clear and fully compliant, so you can fully benefit from the advantages of the Maquila regime.

hello@myparaway.com

© 2026. All rights reserved.

Follow MyParaWay